Screenshots

Problem Statement

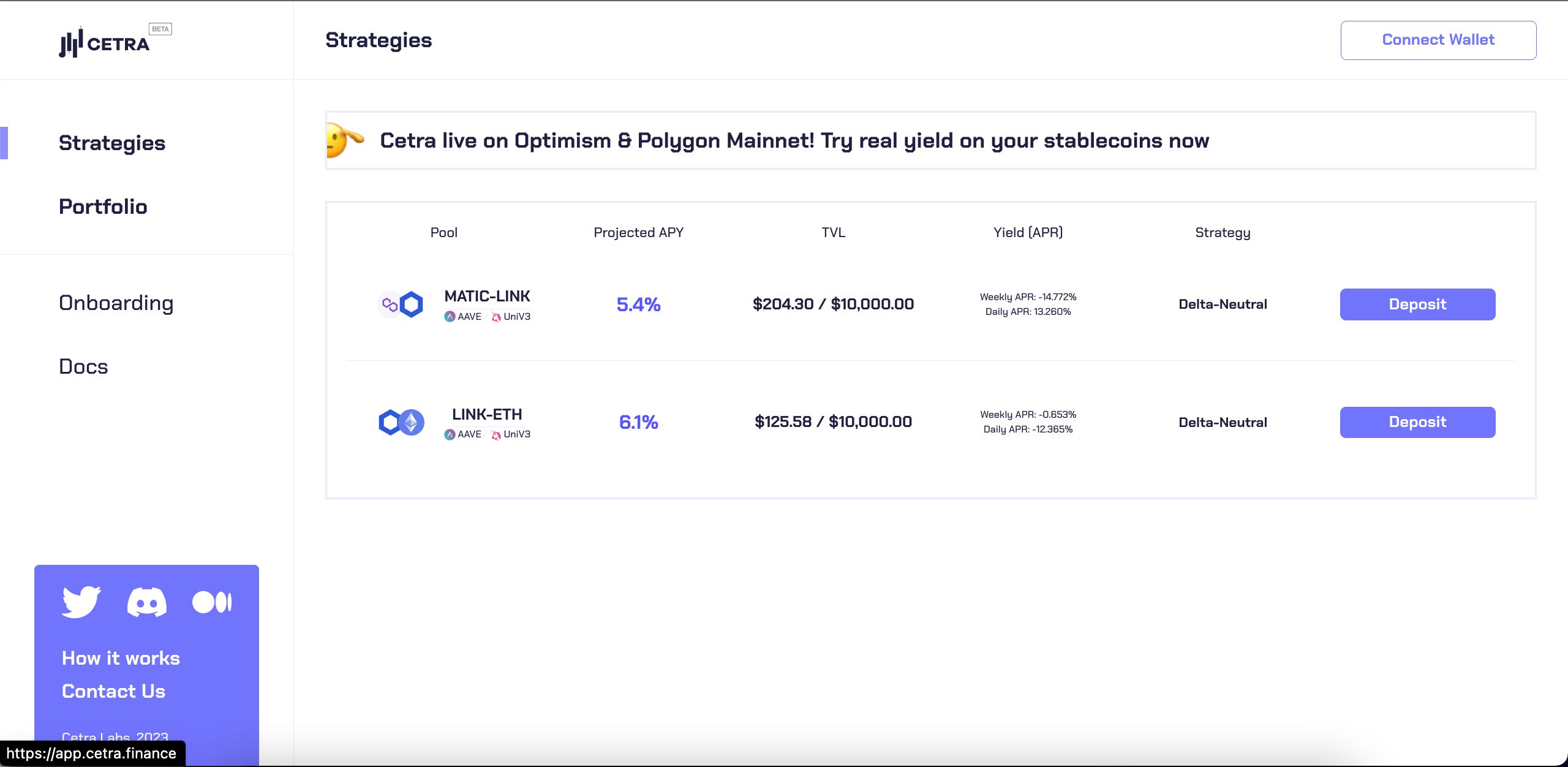

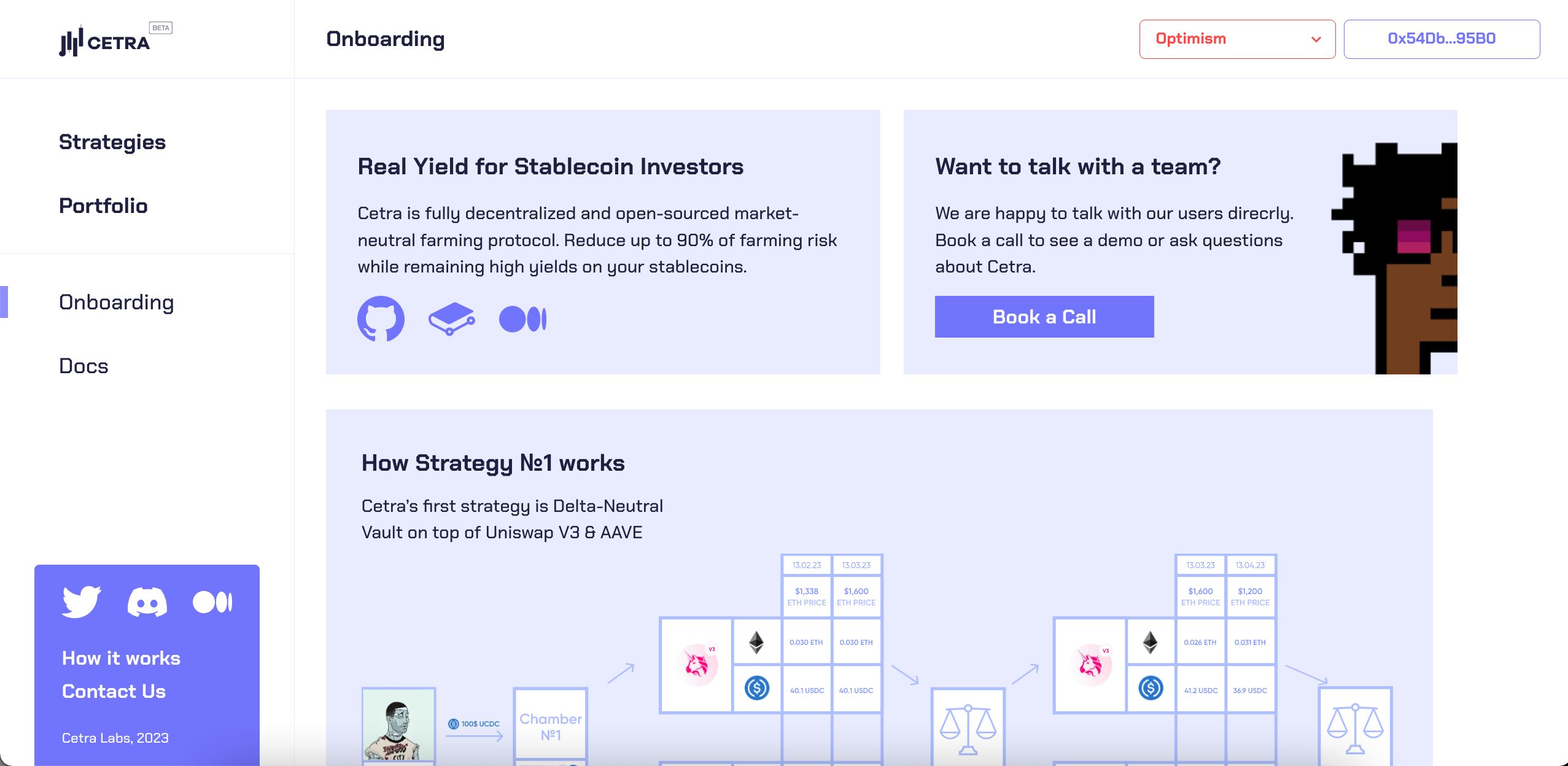

We reduce 90% of DeFi market-making strategies' risks, bringing stability to financial markets and reliable yield to investors. Our vaults offer simple creation, automated hedging and range management of complex on-chain UniV3 market making strategies.Some of Cetra's innovative features are:Portfolio approach to IL management (Omnipool product)Increased hedging capabilities (Custom money-market optimized for hedging "long-tail" tokens)

Solution

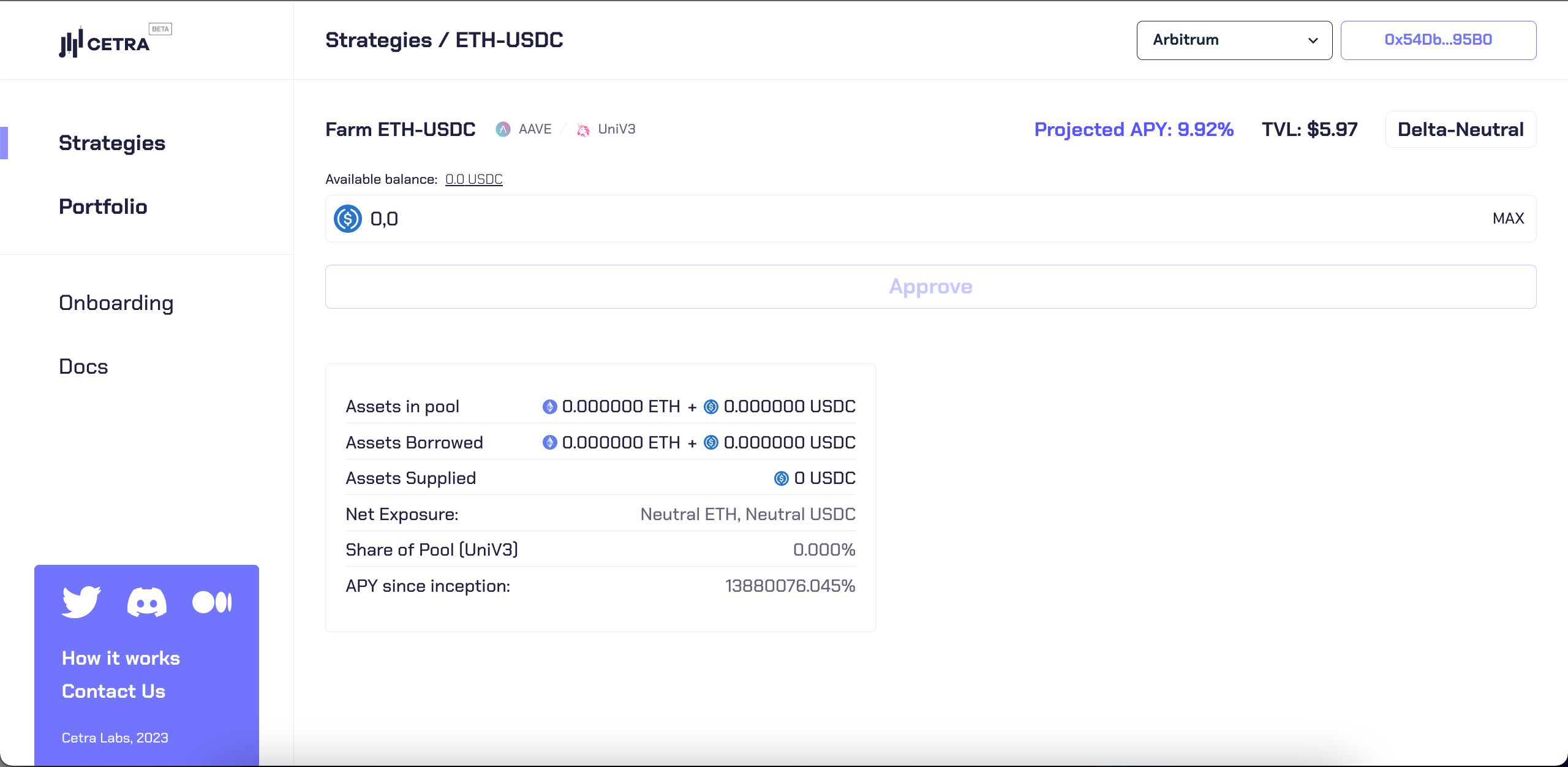

This project uses UniV3 and AAVE to create PDN strategies on Polygon, Optimism, Arbitrum. Rebalancing mechanics works with Gelato & ChainlinkYou can think of the position in terms of 3 “sub-positions”: We own S USDC as collateral and owe X WETH tokens and Y WBTC tokens to aave. We own X +- dx WETH tokens and Y -+ dy WBTC tokens that are kept in UniV3 pool. Amounts dx and dy vary due to AMM design: the variability in essence causes Impermanent Loss. We receive F — trading fees from UniV3 pool, L — lending return and need to pay I — borrowing interest. Usually revenue F + L significantly outweights expenses I.Due to Cetra’s rebalancing mechanism, dx and dy IL variations are kept small and on position closing we own in pool almost exact X and Y to repay the debt (fee revenue is partly used to compensate the shortage). After repaying we can redeem back our collateral S plus remaining fees converted to USDC, and enjoy the USD - notioned yield.

Hackathon

Scaling Ethereum 2023

2023

Contributors

- ortomich

69 contributions

- isumanov

26 contributions

- bezrazli4n0

1 contributions